The global financial system was not designed to exclude the developing world. It was designed for the markets it already knew. The result was a structure where geography became the most consequential financial variable in most people’s lives. A salaried worker in the Philippines, Nigeria, or Pakistan produced output that contributed to global GDP, paid taxes, and consumed goods tied to markets she could not access. The NYSE opens at 9:30am Eastern Time. It closes at 4pm. It requires a brokerage account that requires a compatible national ID, a linked bank account, a minimum balance, and a compliance process written for a specific set of countries. Most of the world did not qualify.

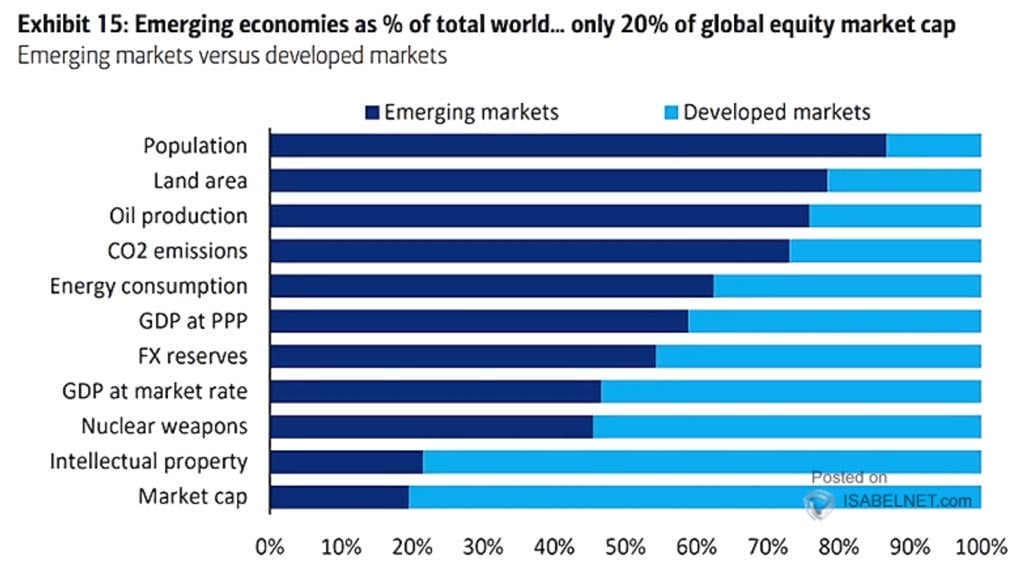

The numbers are not subtle. Excluding China, developing countries represent roughly 12% of global equity market value and around 6% of global bond issuance, despite accounting for more than 40% of world output. Advanced economies borrow at 1 to 4%. Emerging markets pay 6 to 12% for equivalent debt. The same gap that exists in borrowing costs exists in investment access — the price of geography, charged to people who had no say in where they were born.

The infrastructure that built this gap was not a policy. It was a default setting. In 2025, it started being replaced.

What changed

In June 2025, Robinhood launched over 200 tokenised US stocks and ETFs on Arbitrum, available commission-free to more than 400 million people across 30 EU and EEA countries. No opening bell. No minimum balance. By year end, that catalogue exceeded 1,000 tokens. Kraken followed in September with xStocks — tokenised equities on Solana – available across 140 countries. That same month, Ondo Finance opened Ondo Global Markets on Ethereum, 100+ tokenised US stocks and ETFs explicitly built for non-US investors across Asia-Pacific, Africa, and Latin America. It became the largest tokenised securities platform globally within 48 hours of launch, crossing $350 million in TVL and over $60 billion in cumulative trading volume within months.

BlackRock’s BUIDL fund — tokenised institutional-grade yield – has crossed $2.8 billion. Franklin Templeton runs tokenised money market funds on public blockchains. JPMorgan has processed trillions in repo transactions on-chain. The institutions that built the traditional access barriers are now building on top of the infrastructure that removes them.

A wallet address has no nationality field. In permissionless on-chain markets, it executes trades without checking your country of residence.

“More people gained access to US equity markets through onchain infrastructure in 2025 than through traditional brokerage expansion in the previous decade.”

The permissionless markets

The most significant structural development is not tokenised stocks on a regulated exchange. It is the emergence of permissionless market infrastructure — the ability for any asset to be made tradeable on-chain without requiring an institution to sponsor it.

Hyperliquid’s HIP-3 protocol, which went live in October 2025, functions as a permissionless market factory. Anyone can create a perpetual market for any asset by staking 500,000 HYPE tokens. Deployers receive 50% of trading fees. The protocol takes the rest. No listing committee. No geographic restriction on who trades. No market hours.

The open interest on HIP-3 grew from near-zero to over $2 billion in under a year. As of this week, it has crossed $2.2 billion. Trade.xyz – built by Hyperunit, Hyperliquid’s tokenisation arm — holds $2.17 billion of that, around 90% of the total market. On March 18, S&P S&P Dow Jones officially licensed the S&P 500 index to Trade.xyz. Day-one volume exceeded $100 million. It ran through the weekend.

What is trading on HIP-3 is instructive. WTI crude oil generated $1.27 billion in 24-hour volume. Brent crude hit $1.04 billion. Silver crossed $1 billion. These are not crypto-native assets. They are the commodities and indices that have always moved global wealth — now trading 24 hours a day, seven days a week, accessible to anyone with a wallet, with no intermediary deciding whether your geography qualifies.

The S&P 500 no longer has a closing bell for everyone. Crude oil does not check your passport. The market is open.

What this means for policy

The shift happening here is not incremental. It is a redesign of who the financial system is built for.

Every regulatory framework built around capital markets was designed with a specific assumption: that access would be mediated. A broker, a custodian, a licensed exchange — an institution sitting between the investor and the asset, deciding who qualifies. That intermediary layer was also where geographic restriction lived. Remove it, and geography becomes irrelevant by default.

For policymakers in emerging markets, the question is no longer whether their citizens can access global capital markets. They already can. The question is whether the regulatory infrastructure exists to make that participation safe, taxable, and economically productive for the country, rather than happening in a grey area that governments have no visibility into.

The countries that move fast on this do not just protect their citizens. They attract capital, they build institutional capacity, and they position themselves as participants in the financial architecture being built right now rather than observers who catch up later. The window for that positioning is not permanent.

Geography determined access for two centuries because the infrastructure enforced it. The infrastructure has changed. The policies need to catch up.