Oil. Natural gas. Rare earths. Each one followed the same trajectory. Physical scarcity first. Then commodity pricing. Then, futures markets. Then, institutional allocation at scale. The cycle compressed each time. What took oil a century, gas did in 40 years. Rare earths in 20.

Compute is on the same path. We are, right now, at the inflection point between commodity and futures. The window to build the infrastructure layer for that transition is open. It will not stay open for long.

The numbers that prove scarcity

The demand signal has been visible for anyone paying attention.

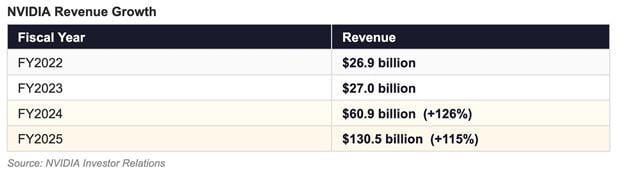

That is not a software company scaling on zero marginal cost. That is a physical resource becoming industrial. The same revenue trajectory appeared in oil in the early 1970s, in rare earths in the early 2000s. The pattern is the same. The compression is faster.

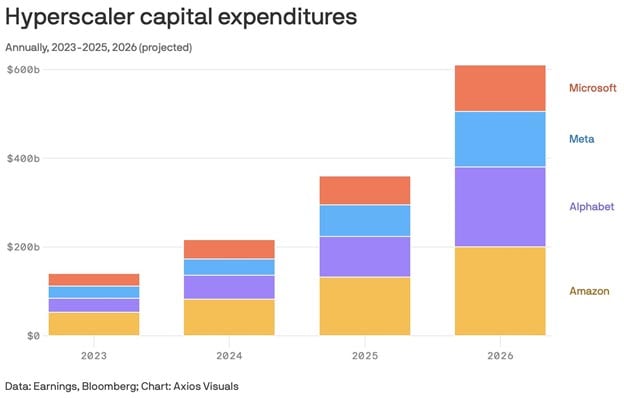

The four largest hyperscalers spent a combined ~$410 billion on capital expenditures in 2025. 2026 guidance has now surged to $700-725 billion (Microsoft ~$190B, Amazon $200B, Alphabet $175-185B, Meta $125-145B). Goldman Sachs now models $765 billion in annual AI CapEx in 2026, scaling to $1.6 trillion annually by 2031 (cumulative ~$7.6 trillion from 2026-2031).

When demand consistently outpaces supply and buyers pay premiums to jump the queue, you do not have a product market. You have a commodity market with price discovery beginning.

In 2023, the lead time for a single NVIDIA H100 GPU was 8 to 11 months. Spot prices reached $40,000 per unit against a list price of $30,000. Supply rationing. Premium pricing. Queue jumping. This is exactly what oil looked like in the early 1970s.

The signal from the establishment

As recently as May 5, 2026, Larry Fink, CEO of BlackRock, managing $13.89 trillion in assets, stated publicly that surging demand for computing power could create an entirely new asset class centered around compute futures – specifically that “a new asset class will be buying futures of compute,” citing shortages in power, chips, and compute capacity.

Fink has form here. He was early on bond ETFs. He was early on ESG as a capital allocation framework. When he speaks publicly about an emerging asset class, he is describing a product pipeline, not an opinion.

The oil futures market took 10 years to form after the 1973 OPEC supply shock. NYMEX crude oil futures launched in 1983. That market now trades $1.5 to $2 trillion in daily volume. The infrastructure around it, the exchanges, the derivatives desks, the storage operators, the financing vehicles, created more sustained wealth than many of the oil producers themselves.

Compute already has its 1973 moment. The H100 shortage of 2023 was a supply shock. The futures contracts are the next step. The exchange that lists them does not exist yet.

Compute is geopolitical

The rare earths lesson is the clearest parallel.

China controls 60% of rare earth mining and 85% of global processing capacity. In 2010, in a territorial dispute with Japan, China cut rare earth exports. Japanese manufacturers were paralysed within weeks. The strategic logic was identical to the 1973 oil embargo: whoever controls the resource controls the leverage.

The United States applied the same logic to compute in October 2022, imposing chip export controls on China’s access to advanced AI accelerators. Those controls were expanded in 2023 and again in 2024. This is resource denial policy. The same strategic framework that shaped 50 years of oil geopolitics is being applied to silicon within a single decade.

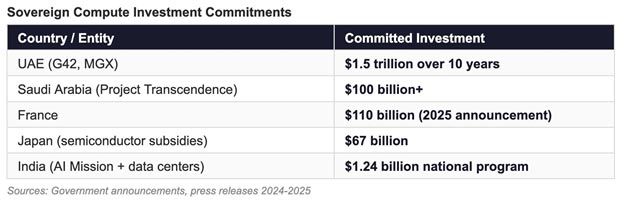

These are not technology investments. They are sovereign resource strategies. The countries building compute infrastructure today are making the same structural bet the Gulf states made on oil in the 1970s. They are acquiring the resource before the futures market forms, before the institutional allocation cycle begins.

TSMC manufactures approximately 92% of the world’s advanced foundry capacity below 10 nm (and the overwhelming majority below 7 nm / 3 nm). The entire fabrication capacity sits in Taiwan. That concentration risk makes OPEC look diversified.

The market forming from both ends

Financial markets do not wait for permission. The infrastructure of a futures market for compute is being assembled without a central exchange.

AWS, Azure, and Google Cloud already operate what is functionally a spot market. Prices fluctuate by the hour. Buyers time purchases around demand cycles. Supply is rationed during peak load. The mechanism of a futures market is present. The standardised contract and the exchange are missing.

CoreWeave went public in March 2025, the first pure-play GPU cloud infrastructure company to list. It reported $1.9 billion in revenue for 2024 (growing to an estimated $5.1 billion in 2025) and priced at a $23 billion valuation at IPO. The market priced it as infrastructure, not software. Infrastructure companies trade on long-term contracted cash flows. The market is telling you what it thinks compute is.

From the other direction, decentralised compute networks are also running early experiments in tokenised compute. Fragmented and early, but directionally correct. They are building price discovery mechanisms for a resource that does not yet have a standardised futures contract. This is what proto-markets look like before the exchange arrives.

The picks-and-shovels opportunity in every commodity cycle is not the resource itself. It is the infrastructure that prices, trades, moves, and finances it.

The agentic shift changes the demand curve

There is a second-order dynamic that makes the compute case more urgent than the oil parallel suggests.

When oil demand grew, it grew at human speed. Cities expanded. Transport networks scaled. Consumption moved with population. Compute demand is now growing at machine speed.

AI agents do not sleep. They do not have office hours. As autonomous systems proliferate, agents managing workflows, executing transactions, building other systems, the demand for compute decouples from human activity entirely. Machine-to-machine work runs continuously. The demand curve loses its nights and weekends.

Every significant deployment of agentic AI adds persistent, continuous compute consumption. The energy and infrastructure requirements scale with the number of agents in operation, not the number of humans using them. The projections being made today, including Goldman’s $1 trillion figure, are almost certainly underestimates of where the demand curve goes when autonomous systems are the primary consumers.

Anyone building at the infrastructure layer right now is sizing a market that will look fundamentally different by the time their infrastructure is operational. The demand projections being cited today are almost certainly the floor, not the ceiling.

What this means for builders

Every commodity cycle creates two kinds of wealth. The first comes from owning the resource. The second, and larger, comes from building the infrastructure that prices, trades, moves, and finances it. The oil services industry created more sustained wealth than many of the oil producers themselves, because they owned the layer beneath the commodity through every price cycle.

Compute is at the same juncture. The financial layer does not exist at scale. No standardised compute contracts. No hedging instruments for companies running large inference workloads. No capacity markets letting buyers lock in future access the way airlines lock in jet fuel. No sovereign compute reserves.

Each of those gaps is a construction opportunity. But the more important dimension underneath all of it is labour. Hundreds of millions of people in markets like Pakistan, Nigeria, and Indonesia built real livelihoods on digital platforms. AI agents are going to absorb a significant share of that task-based work. The question is not whether that happens. It is whether the countries affected own any of the infrastructure that replaces them, or whether they watch the productivity gains accumulate somewhere else.

The first internet made that mistake. The value creation was global. The value capture was not. Compute infrastructure is the chance to build differently. The builders who see it clearly are not betting on a technology. They are making a structural call on the most strategic resource of the next decade.

The window

The scarcity was real before Fink named it. The institutional recognition is now arriving. The financial architecture is being assembled from both ends, cloud spot markets above and tokenised compute networks below, with no standardised exchange in the middle yet.

That gap is where the next infrastructure layer gets built. Every input needed already exists: the demand is proven, the sovereign capital is committed, the proto-markets are forming, and the builders who understand what is happening are moving. The exchange does not exist yet.

The countries and builders who move now will not just participate in what comes next. They will own the rails it runs on.

The opportunity to capture that value is massive.